![]()

We only get to do things Once, is one of Singer/Songwriter, Liam Gallaghers latest tunes on his new album Why Me, Why Not and when it comes to Mortgage Finance using Thai properties as collateral, it could also be said of the same if wanting to build a portfolio of investment properties under finance.

The aim from a buyers perspective may be to pick up several condo units or villas often within the same project and rent them out for a passive income however, if things are not done correctly the first time and once only, it could end up being a nightmare, particularly if overstretched on loan installments and rental income takes longer than anticipated or, doesn’t quite receive the amount of rent one was hoping for. There are however solutions to try and help minimise monthly debt obligations.

A classic type of Mortgage Finance will involve a repayment term over a selected number of years, with an agreed amount paid each month until the end of a contract. In the final year, said loan is paid off in full with the final installment (being the same as all other payments or less), the buyer would then be deemed true owner of said property. This is the most popular and common way of doing finance around the globe with many banks considering this a traditional format.

An alternative that is available and sometimes doesn’t get much real coverage being misunderstood is the balloon payment contract whereby monthly installments are reduced and a final lump sum payment at the end of contract is required. When the average borrower hears about a big lump sum final payment or a loan still having a big payment to make at the end of a contract, it tends to be shut down as an option early on, without fully understanding the benefits of such flexibility.

The key to understanding why a balloon payment term is great can be found within typical lenders criteria to lend in the first place and whether they have flexibility in their product for overpayments. Typically a Mortgage lender will follow some kind of income multiple analysis to decide how much they could loan to any particular borrower. It is not uncommon that monthly income from a borrower should be at-least 3x of the total monthly debt obligations. i.e. If the loan installment is THB 50,000 per month, then it is preferred to have paper trail evidence in the loan approval request of THB 150,000. Multiple income sources can be used, however, it is preferred to be at the 3x level or more. In addition, a lender will often include a borrower’s total debt exposure within calculation therefore, if within a credit bureau report it can be shown a borrower has loans elsewhere or monthly debt obligations such as a car loan, those will also be taken into account which could result in a lower Mortgage being offered since a borrower already has monthly debt commitments.

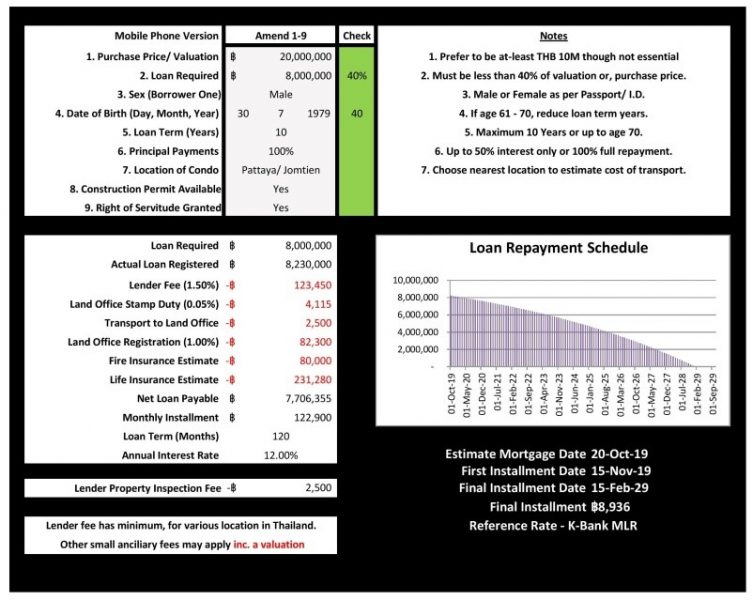

Here is the beauty of a Balloon Payment contract. The final balloon is generally NOT, considered to be a monthly debt obligation, therefore, by saving a lump sum for the final day, an investor lowers the total monthly debt obligation in the loan approval and thus allows for greater amount of loan exposure to be had in the first place. Take for instance the example THB20,000,000 Villa purchase enclosed. The monthly installment on a 10-year loan is THB 122,900 which means THB 368,700 of income evidence is preferred. By choosing a balloon payment of 50%, this lowers the installment down to just THB 106,100 which means income evidence of THB 318,300 is preferred; this is THB 50,400 less than the classic repayment option. If the borrower’s income is only THB 320,000 than this is the difference between a loan approval or rejection.

As an additional extra, what if a borrower has the ability to make bonus payments as and when funds become available, the loan can still be cleared at the same time. i.e. Maybe the borrower has plenty of income but prefers to keep their monthly debt obligations as low as possible with a balloon just in case rental on the property takes longer than expected OR goes for a spell without any income. The borrower can in effect choose, to pay more onto the loan as and when they require rather than the lender demanding installments are paid each month. If as a borrower one overcommits on the monthly installment purely because they wish it paid off as soon as possible, this will often lead to an issue with a lender at some point since generally few can plan for 10 years of consistent income and enough to repay the loan every month. Going back to the 20M example above, there is nothing to stop the borrower from taking the THB 318,300 option and then “choosing” to pay extra each month to the lender of THB 50,400. It would still be like a 10-year traditional repayment loan however the borrower chooses to repay enough rather than is required to pay enough by the lender.

Let’s now consider to look at an investor wanting to pick up several properties under finance thus maximising the amount of leverage possible. It is almost always preferred to take out a balloon payment term since lowers the debt obligation, is more likely rent will cover the Mortgage and it is possible to make lump sum payments from perhaps other property sales in order to reduce the loan as and when required. It is easier to approve more loans to purchase more properties using balloon payment terms.

At MBK Guarantee co., ltd. we have flexible repayment options for both condominium and villa purchases and of course, offer balloon payment terms. Early repayment is possible at any time with only a 2% penalty applied in the first 3 years, after which no penalty is applied. Interest rates on equity release condo loans are around 9.65% and on Villa, purchases are 12%. Terms are available up to 10 years tenor which ultimately if one chooses a 50% balloon payment could mean the borrower is entitled to a 20-year loan (10 plus 10). Loan contracts are dual Thai & English Language with Chinese marketing literature and loan calculators available. Monthly direct debit facilities are used to collect monthly installments and for those who choose to pay extra each month, a simple remittance to our company account at any point with a copy of the deposit slip is required. No advance notice is generally needed however a copy of the deposit slip must be provided.

Back in 2009/2010 when the product was launched, it sent a “Shockwave” around the Property Finance market in Thailand and continues to be “Alright now”, after all these years. “The River” of baht finance continues to “Be Still”, freely flowing for those who wish to apply.

For further information on how to “Finance Property, Land & Condos in Thailand”, or a web-link to the “Thailand Condo Finance Map” which shows pre-approved condominium projects for finance, please feel free to email [email protected] OR, call 66 (0) 81278 5382 OR, Line ID stuartmaxwellfoulkes, I shall then be happy to assist. To speak with a native Chinese national, contact Rose on 66 (0) 95648 2913 or WeChat: rose215620 or email [email protected].